Shield your money and go for windfall profits as major economic cycles converge to create one of the biggest bubbles and busts of all time.

by Martin D. Weiss with Sean Brodrick

In this report:

- Stunning predictions for 2021—2026 from Martin Weiss and Sean Brodrick — “The nightmare that keeps us up nights.”

- 14 Supercycle investments set to multiply your money — 500% profits available NOW …

- Investments designed to pay you up to 50-times more than other investors earn …

- Urgent preparation to protect your wealth and profit. (Click here to jump to this chapter.)

- Immediate access to our “buy” and “sell signals EVERY DAY throughout this crisis. Click here.

Introduction

The End of an Era

Dr. Martin D. Weiss, founder of

the Weiss Companies

As I write these words, the strongest historic cycles known to science are converging — forming a giant supercycle.

It will bring together four sweeping financial cycles with the rising cycle of war. And it will have enormous power.

When cycles like these came together in the late 1920s and early 1930s, the world erupted into an historic speculative bubble and then plunged into a Great Depression that lasted more than a decade.

This time around, they will trigger the end of one major epoch in human history … and the beginning of a terrifying (and enormously profitable) new one.

[To learn about the investments we recommend, jump to this chapter.]

Of course, no one can predict the future with precision, and all investing involves risk.

But the forecasts and profit estimates in this report are based on nearly 100 years of cycles research, giving me a high level of confidence in what I’m about to say …

No matter what decisions our leaders may make, the age we have all known all our lives an era in which governments amassed $300 trillion in debts and obligations— is about to end.

And a new era — the age in which all of us will pay the price for our leaders’ reckless spending schemes and the obscene debts — is about to begin.

We will witness the collapse of the economies, currencies and investment markets that have been built on those debts …

Everything about how you earn, spend, save and invest your money — and about how you live your life — will be altered forever.

In this report, Weiss cycles specialist Sean Brodrick and I show who, why, when … and what to do.

Chapter 1

This Is Your Moment of Truth

What you do in the next few minutes, hours and days could determine your financial destiny for the rest of your life.

So, if you want to get access to our urgent “buy” and “sell” signals starting RIGHT NOW, click here to skip ahead to Chapter 7.

Our forecast is clear and unhedged: We are in for five years of chaos in the global economy, turmoil in world markets, and spreading conflicts — all of which will impact your investments and personal lives.

As this supercycle courses through the world in the months ahead, the lenders and investors that governments count on for loans will snap their wallets shut.

Smart investors are already reading the handwriting on the wall. The clouds of war are turning darker. And even if a single shot is never fired, governments are getting set to ramp up their defense spending like never before. Bloated budget deficits will be bloated even more.

But government debt is already too massive. It can never be repaid. It would be financial suicide for investors to continue loaning their money to Tokyo, London or Washington; insane to throw good money after bad.

So, governments — including our own — will simply run out of lenders, and then … run out of money.

More than 39 million government employees and contractors of the most indebted governments of the world will find that their paychecks have been postponed or cancelled altogether.

Over 300 million more worldwide who depend on government retirement plans like Social Security and health programs like Obamacare will awaken to the same disturbing reality.

And hundreds of millions across the globe who count on welfare, food assistance and other government-sponsored social programs will find themselves unable to feed themselves or their families.

As the news reverberates, currencies, bonds and other investments will simply collapse. The wealth and retirement savings of generations will be vaporized in the twinkling of an eye.

Angry citizens will take to the streets. Local, state and even national law enforcement officials will be overwhelmed. In several countries, law and order will break down, as riots erupt. No person’s life or property will be safe.

Before it’s all over, many governments (equally desperate to survive) will have no choice but to confiscate wealth from their own citizens. Our world, and ultimately, our own nation will be changed forever.

Admittedly, this is the most severe

warning we have ever issued.

Make no mistake: I fully understand just how shocking this forecast is.

I also understand that, with a recovery from the Covid crisis now unfolding, most people who hear it will dismiss it as being “too extreme.”

That’s to be expected.

It’s what happened when we warned that the stock market was about to collapse in 1987 …

It happened again when we warned that tech stocks were due to crash in 1999 …

And it also happened in 2007 when we told anyone who would listen that the U.S. real estate market was about to plummet, plunging the economy into one of the most severe recessions ever.

But please understand, this is no idle prediction. We have no interest in frightening anyone. We are simply following our research to where it takes us.

And it is taking us to a terrifying place. Those who are unprepared for this great crisis risk losing everything: Your income, savings, investments, your properties, your personal and financial security are all at risk.

We do not want that for you.

To warn investors of crises like these is the main reason I founded my company 50 years ago.

It’s why I hired renowned cycles experts Larry Edelson and Sean Brodrick more than two decades ago. And it’s why we’ve written this urgent report for you right now.

The plain truth is, the most powerful cycles forecasting tools we have ever used are virtually screaming that all hell is about to break loose, globally … in Japan … then in Europe … and ultimately right here in the United States.

Chapter 2

The Predictive Power of Cycles

If all of this is hard for you to believe, I certainly understand. After all, despite the dangerous chain of events we’ve been writing about, things still seem pretty much OK today. But the fact is …

The same forecasting tools that accurately predicted the Roaring 1920s, the Great Depression — and every major economic event since …

Are now warning that we’re headed toward the most severe financial crisis any of us has ever seen.

It may help you to understand why I trust this research so completely. Or why I am changing everything in my own financial life to prepare for the events it predicts.

U.S. President Hoover’s chief economic advisor, Edward R. Dewey, discovered the power of these cycles in 1932.

Our forecasting tools are not new.

Some were discovered by Russian economist Nikolai Kondratieff in 1925.

And the balance were developed by an American economist a few years later.

The year was 1932. That’s when U.S. President Herbert Hoover ordered one of his economists, Edward R. Dewey, to determine what caused the Great Depression.

What Dewey found was shocking; he found very powerful economic cycles that govern the rise and fall of economies, currencies and investment markets.

It made perfect sense: All of creation moves in cycles — from the lifecycle of stars, the ebb and flow of the tides, changing of the seasons, human respiration and even to our beating hearts.

Just as cycles govern the physical universe and our physical bodies, they also govern the affairs of man — including the rise and fall of empires, nations, societies, economies, currencies and investment markets.

All of these things and many more are ruled by regular, PREDICTABLE financial cycles.

Dewey’s ultimate conclusion was a shocker: Anyone who studied the charts depicting these cycles could have known about the approaching Great Depression well in advance.

The Depression happened because it was TIME for it to happen.

Cycles research has accurately predicted

nearly every major financial event in our lives.

As the founder of my 50-year-old company and the man who has worked so closely with our cycles experts for so many years, I know. Their knowledge of cycles is what allowed us to accurately warn of the 1987 and 2008 stock market crashes well in advance ... along with nearly every major move in U.S. stocks since then.

Our team of cycles analysts is robust: Larry Edelson, who passed away in 2017, was the first.

Sean Brodrick, who worked closely with him for over a decade, was the second.

Juan Villaverde, who has built a complex computer forecasting model based on cycles, is the third.

Sean, in particular, is proudly the first person in our research group who introduced us to what he calls “The Great Supercycle.”

And he has predicted cycles with amazing accuracy. Plus, he and I worked very closely together to write this report.

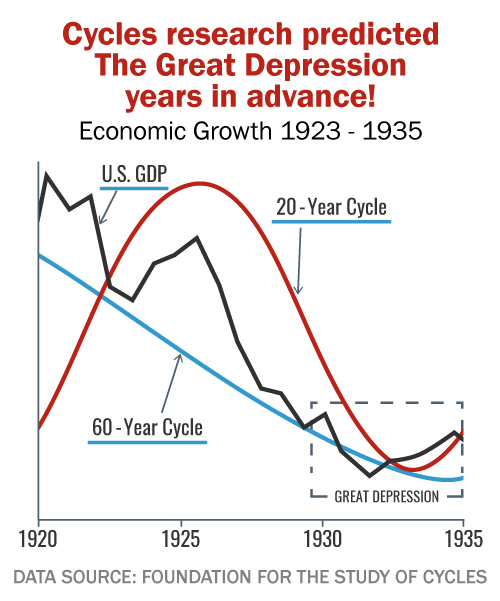

Take a look at the chart to the right, an example of our work. It is the product of our cycles research in 2006 and 2007 — work we did well before the U.S. real estate market cracked.

The red line is the cycle we were following — the cycle that helped us predict a major catastrophe ahead.

The black line is what actually happened.

As you can see, the cycle clearly predicted that the U.S. economy would peak in 2007, then suffer a massive crash.

Edelson Institute’s

Sean Brodrick

Our cycles research has made it possible for us to accurately predict …

- Every major move in the stock market since 1986 …

- Every major trend in the gold market since 1999 …

- Major movements in the U.S. dollar, the euro and yen, oil and many other commodities …

Predictions that could have helped you multiply your money many times over!

Get our “Buy” and “Sell” signals for today’s best Supercycle investments:

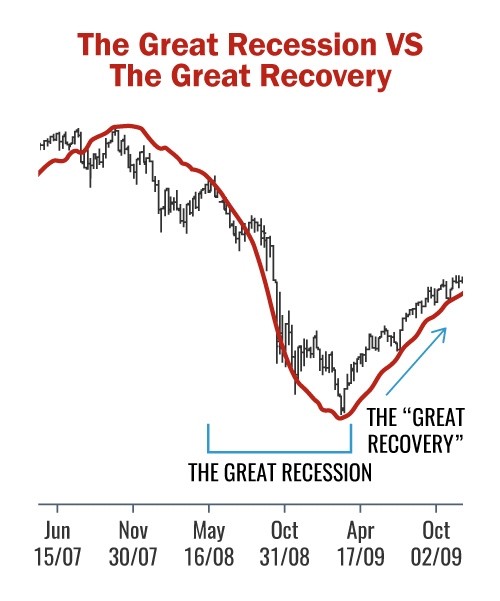

RESULT: The Great Recession of 2008—2009 struck right on time, just as we predicted, and the S&P 500 crashed nearly 60%.

Anyone who bought the 3x inverse ETF of the S&P 500 on our forecast could have seen nearly a 180% gain.

And that’s only the beginning of the story. That same chart I just showed you also predicted that the bottom in the stock market would come in March of 2009. It forecasted that, from that point forward, the economy and the stock market would begin a long-term recovery.

So, on March 16 of 2009 — while other analysts were still licking their wounds and terrified to even touch a stock — our team announced that the worst was over, and that stocks were about to catch fire again.

RESULT: Since that forecast, the S&P 500 is up a whopping 372.9% — enough to turn every $10,000 invested into $47,290.

And if you had used our forecast to invest in the 3x S&P 500 ETF, you could be up as much as 720% — enough to turn every $10,000 you invested into nearly $82,000.

Plus, our cycles research has also helped us call every major move in the gold market since 1999 …

Including the beginning of the bull market when gold was just $255 per ounce … and the end in September 2011 when it hit $1,925.

And that’s only the beginning of the story. That same chart I just showed you also predicted that the bottom in the stock market would come in March of 2009. It forecasted that, from that point forward, the economy and the stock market would begin a long-term recovery.

In 2015, we predicted the world would enter a new era of financial and political turmoil, and it did.

That’s also when we first warned that the end of the European Union was on the horizon. Soon after, millions of migrants flowed into Europe, pushing social services to the breaking point and beyond.

Worse, they are forcing those governments to spend billions of dollars that they don’t have, pushing them deeper and deeper into debt.

Great Britain shocked the world by voting to leave the European Union, while powerful new separatist movements in Greece, Spain, Germany and France pushed the Union to the brink of oblivion.

In 2015, we also warned about flight capital from overseas that would drive U.S. stocks to unimaginable new levels.

As a result, we predicted that the Dow Jones Industrial Average would surge well past the 20,000 mark. Sure enough, trillions of dollars flowed into the United States, and the Dow surged by 6,000 points, topping 22,000 and moving on to even higher levels.

Now, our cycles research is sending us a new message — a signal that no wage-earner, retiree or investor can afford to ignore — the focus of our next chapter.

Chapter 3

Powerful Cycles Aligning Globally

Even as you read these words, we are witnessing a major alignment of the most powerful forces known to man — the same kind of convergence that preceded some of the most disruptive upheavals of modern history:

- The time-honored Kondratieff Wave, which is signaling an Armageddon for massively indebted economies — soaring inflation … defaults on government debts … and more ...

- The rapidly rising cycle of monetary excesses — unprecedented money printing by the Federal Reserve, the European Central Bank (ECB), the Bank of England (BOE) and the Bank of Japan (BOJ).

- The rapidly rising cycle of government spending, deficits and debts — with nothing to back them up, no hope of ever repaying them, and mounting pressure on governments to devalue their currencies.

- A major new cycle of rampant inflation that’s just beginning to rear its ugly head as costs for construction materials, housing, food and energy already begin to surge.

Plus …

- The escalating cycle of war, including the New Cold War, cyber wars, trade wars, currency wars, civil wars, regional wars and more. These conflicts are aggravating the inflation and debt cycles. And they’re also driving a flood of flight capital to safe havens, including the U.S. stock and real estate markets — not to mention gold, and Bitcoin.

The facts on the ground

are especially disturbing.

The facts coming to light right now are not only very disturbing, but they also confirm that each of these cycles are already having a major global impact on the daily lives of billions of people and millions of enterprises.

The Kondratieff Wave began to strike hard in 2008 when the global financial system came to the brink of a fatal meltdown.

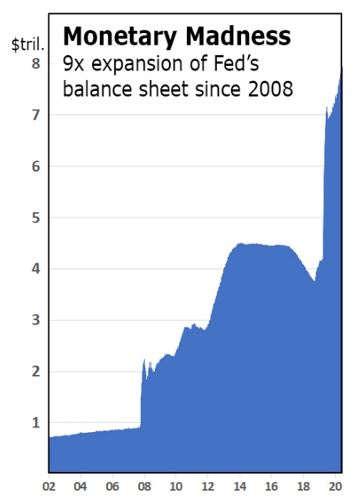

The current cycle of monetary excesses began soon thereafter. That’s when the governments of the U.S., Europe and Japan responded by printing more money, more quickly than any prior governments in history.

The Fed’s monetary madness has been the biggest of all (see chart). Since 2008, it has printed a record-smashing $7 trillion.

The Fed then used that money to buy up $7 trillion in assets and stuffed them into its balance sheet where they still sit today.

The cycle of surging government spending and deficits also began to accelerate at that time. But it truly exploded in the wake of the Covid pandemic. That has prompted the U.S. government to run up a budget deficit of $2.1 trillion in 2021 and trillion-dollar-plus deficits for many years to come.

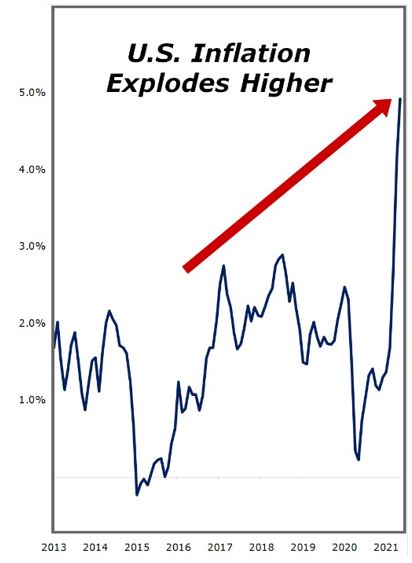

So, it should therefore come as no surprise that the long-dormant inflation cycle is now again rearing its ugly head.

U.S. consumer prices have gone through the roof.

The inflation rate has suddenly jumped to about TRIPLE the average of the last eight years.

And STILL the Fed continues to pump money like crazy …

And STILL the government continues to run up the largest federal deficits of all time.

Sure, government economists pooh-pooh the inflation numbers. That’s what governments always do.

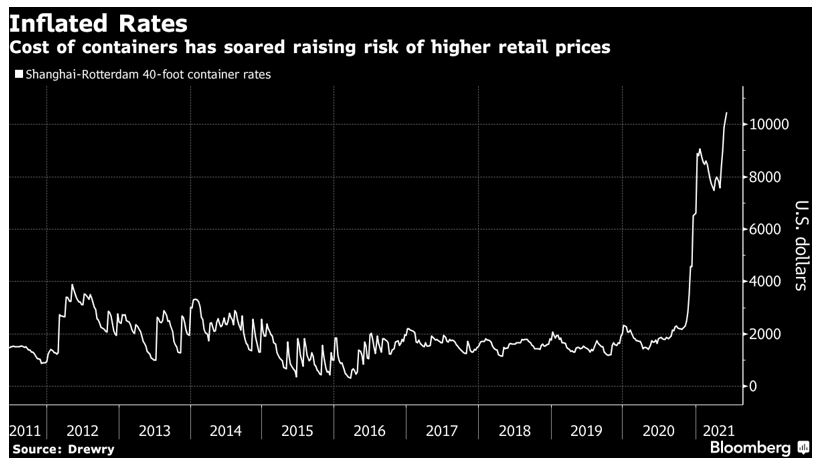

But inflation is not just a domestic problem. Consider, for example, the global cost of shipping goods:

|

For the past half decade, it has rarely cost more than $2,000 for a 40-foot container.

Now, it costs more than $10,000. That’s over FIVE times more. And this alone makes almost everything in the world much more expensive.

We know what’s likely to happen next. Because we’ve seen the cycle of inflation ravage countries from immemorial times.

In my own 50 years studying inflation on the ground, I’ve personally seen it run amuck in many countries and in many different ways.

But I can tell you flatly ...

This is worse.

It’s global.

It’s beyond the power of any government to control.

And it’s just getting started.

The money printing and debt pile-up

in Japan is even worse.

Japan sank into a deep economic depression in the early 1990s.

And for the past three decades, despite the most intensive and persistent central bank money printing in all its recorded history, the economy has been mired in on-again-off-again depressions ever since.

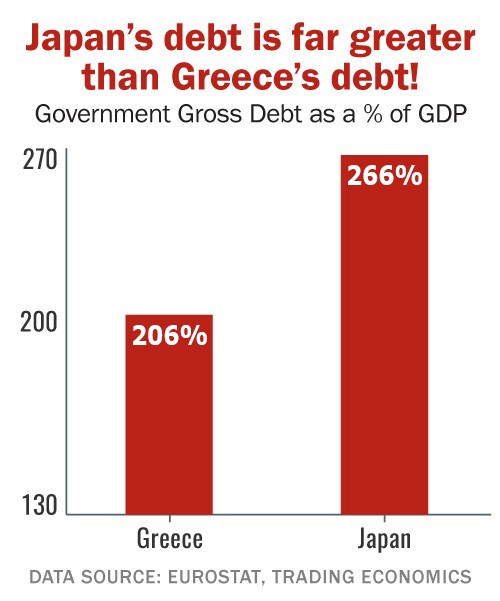

End result: Japan’s government debts are the worst in the world, representing 266% of its GDP. That means that government debts in Japan absolutely swamp their entire economy — to the tune of $2.66 in debt per dollar of economic output.

How does that compare to government debts here in the US?

The total government debt in the U.S. is $26.5 trillion. If we had a debt load equivalent to Japan's, it would be close to $75 trillion.

Most people think we have it bad. But in Japan, it's nearly three times worse.

What's the chance they could pay it down? None.

If by some miracle, Japan could achieve a budget surplus of 1 trillion yen per year, it would still take a staggering 1,500 years to pay off their debt.

I know Japan well. I lived in Japan during its bubble years of the 1980s while I worked as an analyst at one of their largest securities firms. Now, I go there as often as I can to visit my son, who’s been living in Tokyo for over 10 years.

So, I can say without hesitation: I believe Japan is on a collision course with one of the worst fiscal collapses the world has ever seen.

What is Japan doing about it?

Their so called solution is to literally tax people to death. Already, estate taxes are so big in Japan, it's almost impossible to inherit wealth.

For example, I have a dear friend who will one day inherit her mother's home in central Tokyo. It's the home she grew up in, and she wants to keep it in the family. But because the estate tax will be so large, she's going to have no choice but to sell the home to cover the tax bill.

It's the same dilemma for many families in Japan, but that's just the estate taxes. The consumption tax is worse. It was already 8% nationwide and that was bad enough. In recent years, to ward off the looming fiscal collapse, the government jacked it up even further to 10%.

But is the government using those extra tax revenues to pay down its debts? Heck no! They're using it to finance more social programs, especially to support the retired and the elderly, which make up nearly one-third of the total population. That’s DOUBLE the share of the older generation in the United States.

OUR FORECAST: Japan’s already-bulging budget deficit will explode. Debt load will strangle the economy. The bond market will collapse. Plus, for reasons I’ll explain in a moment, exports — still the lifeblood of the Japanese economy — will plunge. The economy will crater. Tax revenues will evaporate.

Get our regular updates to protect and build your wealth as the Supercycle heats …

PLUS, urgent investment recommendations whenever we release them (DAILY when warranted) and much more.

A new European debt crisis is on the horizon.

In Europe in the early 2010s, we saw the cycle of debt strike Greece. Then it hit Portugal, Spain , Italy and Greece again. But what you saw in Europe in the prior debt crisis is just a sneak preview of what's coming.

And again, the numbers support this forecast all the way.

All across the continent, the government burden today is far worse than it was during the last major debt crisis.

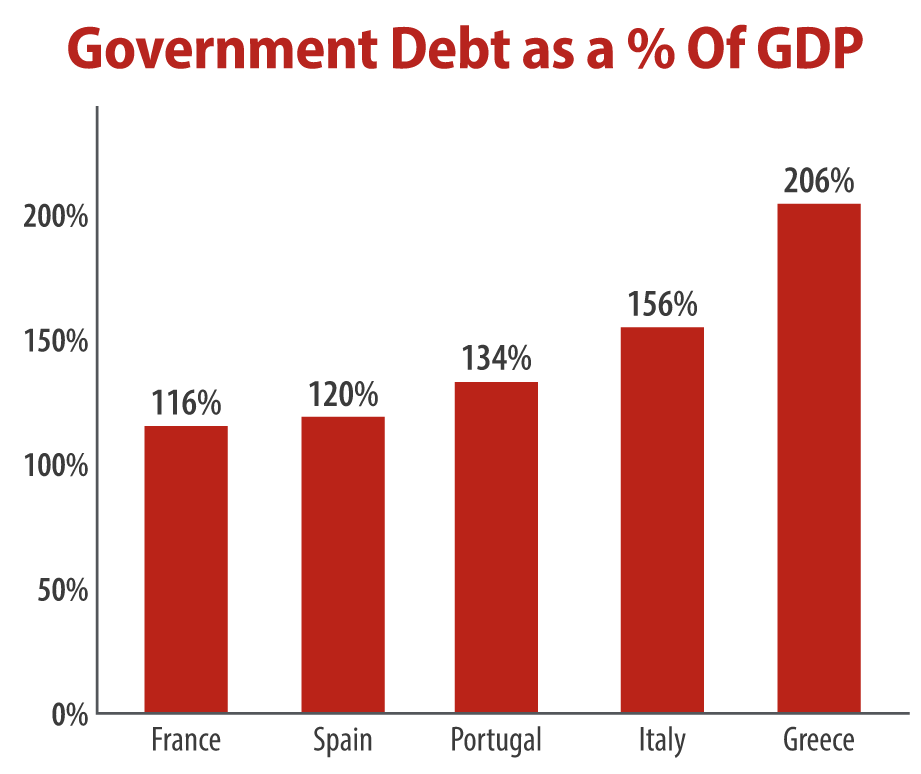

In France, government debts are 116% of GDP. In Spain, they're 120%, in Portugal 134%, Italy 156% and Greece 206%.

|

To get a sense of how bad this is, consider this fact:

Back in the 20th Century, 50% of GDP was considered a dangerous line that no country should ever cross. Now, their debt loads are as much as four times larger.

We're in uncharted territory, which begs the question: Where will be the tipping point?

The answer: banks.

Take the banks of Italy, for example.

They now have more of their capital and reserves tied up in Italian government bonds than at any time in history — even more than they did in the depths of the last financial crisis.

I know this is far away from home. So, let me explain the gravity of this from a historical perspective.

You see, in other countries, when banks have been in trouble, what have they done? They counted on the government to bail them out. But in Italy it's been the opposite. When the government's in trouble, it’s the reverse: It calls on the banks to bail out the government — to buy its bonds.

This is a wild experiment that makes Frankenstein look tame. Any surge in inflation and interest rates could slash the value of the banks’ bond holdings and gut their capital.

All the news most people have seen out of Europe in recent years has been about the immigration crisis, the Brexit crisis, the pandemic crisis and the political crisis.

And it’s true that all of those factors are driving the European Union toward the brink. But in terms of their potential impact on the daily life of average people, nothing compares to the government debt crisis. It will severely impact the lives of 450 million citizens of the European Union.

And it will lead European governments to take desperate measures.

After the last debt crisis, the Spanish government began taxing bank deposits. People paid an income tax on their paycheck, then paid still another tax when they deposit it in their bank.

In France, police routinely searched travelers. They looked for large amounts of cash being smuggled out of the country to avoid taxation.

In Cyprus, the government literally robbed its own banks. Depositors with more than 100,000 euros watched helplessly as the government seized up to 40% of their money.

This time around, expect even more desperate measures.

OUR FORECAST: The European Union will not survive. It will disintegrate. This will serve as a second blow to Japan, one of Europe’s biggest trading partners. And these powerful economic cycles are already converging right now, forming the supercycle that will signal Europe’s future collapse.

Specific “when-to-buy” and “when-to-sell” recommendations to help you

grow richer as the EU disintegrates:

- Investments designed to make you up to six times richer when the euro and European stocks react to this Supercycle, and …

- U.S. investments that could multiply your money as flight capital drives them higher:

Chapter 4

Why the U.S. is the World’s

Safest Safe Haven … for Now

Believe it or not, there is some good news in all of this — especially for investors in the United States.

The first bit of good news is that there’s still time — not much time, mind you, but some time — to prepare.

The second piece of good news is that the troubles in Japan, Europe and other hot spots around the world have wealthy investors seeking safe havens. And at this juncture, the world’s safest safe haven is the United States of America.

That’s why savvy overseas investors recently dumped trillions of yen and euros, driving those currencies lower …

They bought trillions of U.S. dollars, driving the greenback sharply higher. And they used those dollars to buy assets like the following: Stocks. Real estate. Bonds. Even collectibles.

But if history and our cycles research prove anything, it’s that this trickle of flight capital we’ve seen coming to our shores so far is just a sneak preview. It is about to become a massive flood.

It’s crucial that everyone who owns stocks … everyone with a retirement account … understands this.

Because at a time like this — with much of the world burning down around you — growing rich is your only real defense.

And here’s more good news. Our research shows …

This crisis will unfold in three, distinct phases,

giving you the opportunity to amass

not just one, but THREE impressive fortunes:

Investors are delighted when they can make one fortune. But thanks to three entirely separate and clearly defined phases, this crisis will give you the opportunity to build three fortunes:

Fortune #1: Phase 1 — Happening right now, as the Fed continues to pump up the U.S. economy and money continues to flow to the U.S. from the hottest trouble spots overseas …

Fortune #2: Phase 2 — as Japan and then Europe implode, causing the flow of money into U.S. stocks and other investments to flood.

Fortune #3: Phase 3 — when this crisis comes to America, and the United States pays the price for the largest orgy of debt in more than 5,000 years of human history.

Because with each passing day, America’s final reckoning is drawing nearer.

The same fate suffered by Japan and

Europe ultimately awaits us as well.

The bounce from the pandemic, the flood of government spending and the nonstop Fed money printing are boosting the U.S. economy right now.

Plus, the flow of capital from overseas is also a big factor.

But no one can make America’s huge debt problem disappear. And Washington debts are far larger than most people realize.

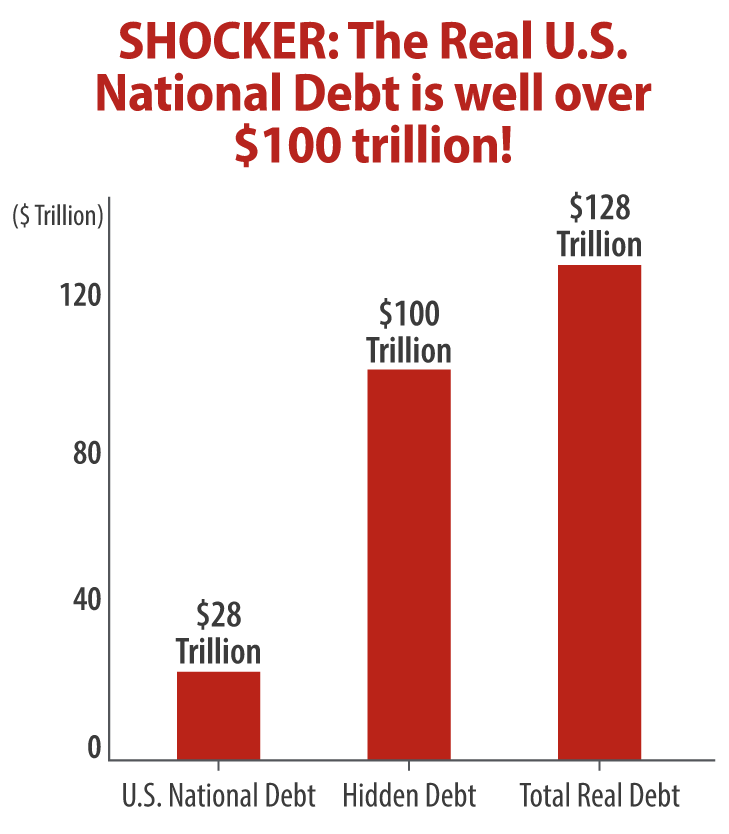

Everyone worries about our $28.2 trillion national debt — that it equals MORE than the value of all the goods and services the U.S. produces.

But let me tell you: That’s a drop in the ocean.

In addition to that debt, according to the latest statistics from the U.S. Treasury Department, our government owes close to another $100 trillion that it never wants to talk about.

These are what it politely calls “unfunded liabilities” — the money it owes primarily to veterans and to seniors for pensions, Social Security and Medicare payments.

Altogether, Washington is on the hook for more than $128 trillion.

That’s nearly six times the size of the entire U.S. economy.

A line of 128 trillion-dollar bills would reach around the Earth at the equator more than 500,000 times. It would reach all the way to the sun and back more than 60 times.

And what’s worse, some economists say the real number is much higher — well over $200 trillion. Plus, hundreds of billions more dollars in additional debt, and obligations are piling up with every passing year.

Sorry, but I have to ask,

Who are we kidding here?

Everyone knows Washington will never make a dent in that debt.

What most economists know, but don’t say, is that Washington won’t be able to even service that much debt for much longer. Any significant surge in defense or welfare spending, or a decline in the economy, could ultimately push Washington into a default of some kind.

It could be a default on the sly (via inflation), a default via a dollar devaluation or perhaps even an outright default forced by a government shutdown.

And long before that happens, U.S. government bonds will have collapsed in value.

The bottom line is that our government, our economy and our society are living on borrowed time. It will all come crashing down.

The great debt collapse

this supercycle brings with it

is as certain as death and taxes.

We’ve always known there was no way Washington could tax, print and spend forever. That kind of insanity is simply unsustainable.

We’ve always known that the day would come when it would all come crashing down. The only question has been “WHEN?”

Now, we have an answer.

Our study of cycles — the most powerful forces in the economic universe — has provided it.

The great global government debt collapse that will begin in Japan … that will spread to Europe … will inevitably strike America as well.

When that happens, only those who are prepared will be able to protect their loved ones, preserve their wealth and maintain their quality of life.

Moreover, those who prepare will have the opportunity to make a lot of money — with the handful of crisis investments that typically explode in value at times like this.

Chapter 5

Preparations to Protect Your

Wealth and Profit

At this moment, we have our eye on three broad categories of investments for the years ahead:

Category A — Assets that cannot be confiscated.

Remember, the coming debt crisis will hit governments. And governments will seek every devious way they can in order to gain control over your wealth, even confiscating assets directly or indirectly.

Ironically, U.S. stocks are among the least likely to be confiscated.

No one is going to take away your shares in the bastions of capitalism — Google, Facebook or IBM. Foreign investors know that.

And that’s the type of asset foreign investors will be chasing.

We first began alerting investors to the massive influx of “fear money” in 2015. And since that time, flight capital has already driven many U.S. stocks through the roof.

If you had owned the right stocks since 2015, you could have seen life-changing gains from that capital flight in just the past two years, such as:

- A 909% gain with Netflix …

- A 1,000% gain with Amazon.com …

- A 1,260% gain with Tesla …

- And a whopping 3,593% gain with NVIDIA, enough to multiply your money more than 36 times over.

And soon, the trickle that has caused these spectacular gains already will become a flood, and the gains we’ve already seen will pale in comparison. If you own the stocks that foreign investors want, you have the potential to rake in a fortune.

Our plan is to own the stocks that foreign investors will be chasing BEFORE they do.

Category B — Alternative assets you should own as hedges against a government crisis — and capitalize on the flood of fear capital.

Gold and silver have served as mankind’s ultimate crisis hedges for 5,000 years. We see gold bullion prices soaring to $6,000 per ounce. That would be more than three times today’s levels. Meanwhile, we see silver going to $150, a five-fold rise from here.

And when bullion prices skyrocket, the shares of companies that produce them go even higher.

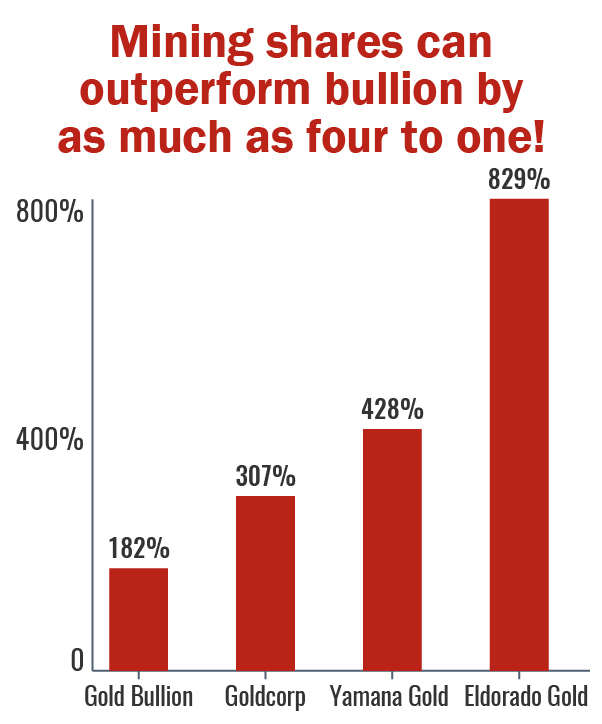

For example, from October 2008 to September 2011, gold bullion prices rose 182%. That means they almost tripled in price.

But if you bought shares in a gold mining company like Goldcorp, you could have seen gains of 307%, or four times your money.

And in Yamana Gold, you could have seen a gain of 428%, or more than five times your money.

In Eldorado Gold, the profits were even better — 829% or more than nine times your money.

Moreover, those remarkable gains posted by the “big boys” of the mining world often pale in comparison to those of small-cap miners — Sean’s particular area of expertise.

Sean has personally visited small-cap miners in Mexico, the Arctic and all over the Americas. He prides himself on getting his boots dirty and investigates these investment opportunities on the ground.

He meets regularly with mining executives from all over the world. And the money those companies have made for investors is even greater than the profits I just told you about.

Small and junior mining stocks to go for

gains of 974%, 1,481%, or even more.

Investing in small-cap miners and developers give you the benefit of leverage that’s just as powerful as the leverage of call options.

But you can do it without any options at all, without risking more than a tiny fraction of your capital ... without using debt or margin accounts ... and without expiration dates.

In other words, no time limit on your opportunity!

Again, history provides the best example.

In the last global debt crisis, which was smaller than the one on the horizon today, gold bottomed at $700 on a pullback and proceeded to rocket to $1,900 over the next two years ... an impressive 171% gain.

But in that same time, the historic data shows that, if you'd been investing in Sean’s favorite junior miners, you could have seen gains like ...

- 324% on Premier Gold

- 455% on Richmont Mines

- 502% on Chesapeake Gold

- 723% on Oceana Gold Corp

- 937% on High River Gold

- 974% on China Gold

- 1,245% on Midway Gold

- 1,481% on Centerra Gold

- 2,295% on Allied Nevada, and

- A staggering 5,237% on Kaminak Gold

That last one is 30-times more money than simply holding gold ... and enough to turn every $500 into $26,685 ... every $1,000 into $53,370 ... and every $25,000 invested into $1,309,250 — on just one stock!

Companies that produce these “white metals”

can give you gains of 566%, 719%, 1,076% and more.

There’s one sector in particular that practically nobody is paying attention to: Industrial metals.

But the convergence of cycles — and the global megatrends born as a result — are driving these metals through the roof.

Sean calls it the “Secret Rally” — and it is part and parcel of the supercycle coursing through the world economy.

Meanwhile, he’s famous for finding companies that produce these metals with the potential to give investors the opportunity for many times those returns.

Consider what happened in the last cycle, for example …

- Solitario Zinc surged 114%.

- Century Aluminum jumped 566% …

- Silver Bull Resources, which is a big supplier of silver and zinc, surged 719% …

- Starfield Resources, a developer of copper and nickel, skyrocketed 1,076%, and …

- Sarissa Resources, which develops copper and uranium, jumped as much as 1,214%.

It’s no coincidence that these companies could have made investors vast fortunes. It’s all part of the supercycle in commodities that Sean first wrote about many years ago. Plus, now …

Metals used for energy are white-hot.

Shortly after the turn of the last century, we saw the world shift from horses to internal combustion vehicles. Now, a similar shift is going on from internal combustion vehicles to electronic vehicles.

Two metals, lithium and cobalt, are integral components of the batteries that power electric vehicles. And now, flight capital from fearful investors — plus rising demand — is expected to drive the price of these metals through the roof.

What if the debt disaster ultimately drives the global economy into a Great Depression?

Well, just because there was a Great Depression in the 1930s, the world didn’t stop switching over from horses to the internal combustion engine. It’s the same thing today.

That’s why the shares in companies that benefit the most from this trend will continue to surge. And flight capital from overseas is turbocharging this trend:

Just since March of 2020, Standard Lithium is up 608%. American Manganese is up 661%. Encore Energy is up 1,255%. And these are not even the biggest winners.

Category C — Leveraged Investments

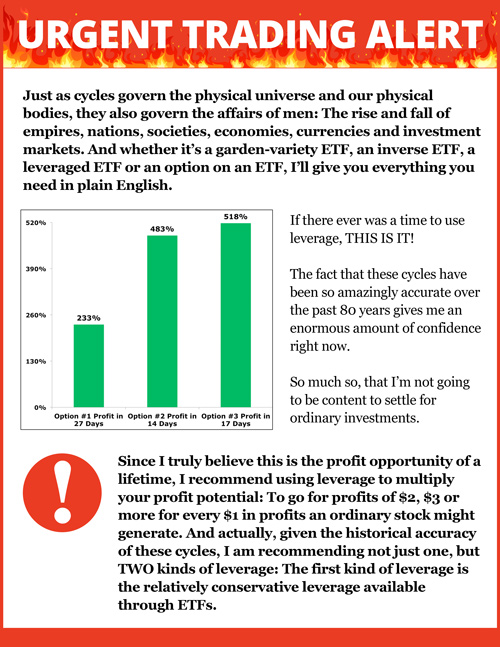

If there ever was a time to use leverage, THIS IS IT!

The fact that these cycles have been so amazingly accurate over the past century gives us an enormous amount of confidence right now.

We’re not going to be content to settle for just ordinary investments.

Since we honestly believe this is the profit opportunity of a lifetime, in special cases, Sean will recommend using leverage to multiply your profit potential: To go for profits of $2, $3 or more for every $1 in profits an ordinary investment might generate.

And given the historical accuracy of these cycles, we recommend not just one, but THREE kinds of leverage:

The first kind of leverage is the relatively less risky leverage available through ETFs.

Many ETFs give you two and three times leverage. So, for every $1 in profit other investors make, you can make $2 or $3. You could make up to triple the profits.

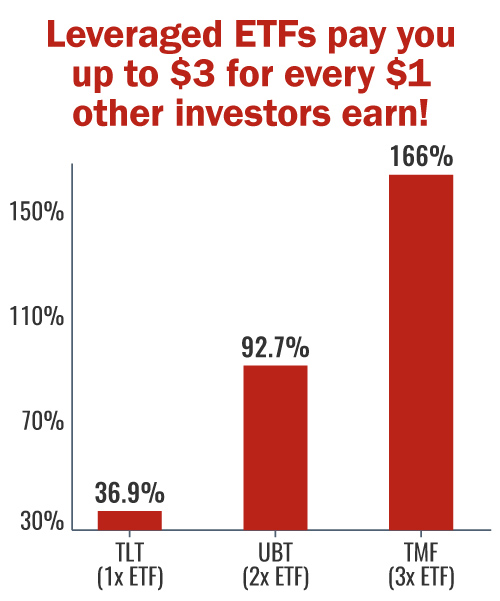

Example: Not long ago, in a just a 13-month period, the “Plain Jane” ETF that owns U.S. Treasuries — iShares 20+ Year Treasury Bond ETF (TLT) — posted a 36.9% gain.

Meanwhile …

The double-leveraged ProShares Ultra 20+ Year Treasury (UBT) produced a 92.7% gain … and the triple-leveraged Direxion Daily 20+ Yr Treasury Bull 3X Shares ETF (TMF) could have made you 166% richer.

Are 500% profits really possible today?

|

Yes — because crisis brings opportunity.

The greater the crisis, the greater the opportunities.

So, this supercycle crisis is the mother of all profit opportunities for investors.

The cycles that make this crisis predictable also gives a huge advantage over other investors …

An advantage I plan to exploit with investments designed to quintuple the profit potential.

CLICK THIS LINK TO JOIN US AS WE GO FOR WINDFALL PROFITS IN 2021-2026

The second kind of leveraged investment we recommend from time to time is somewhat more aggressive. These are options on stocks and ETFs.

I’m talking about buying call options on select U.S. stocks that we expect foreign investors will want to own, and also on ETFs that own those stocks.

This is important since, instead of paying you “only” $2 or $3 for every $1 or profits possible in the underlying investment, options could pay you $10 … $25 ... $50 or more.

Of course, all investments involve risk — and that includes options.

The good news is, it’s not hard to guard against losses with appropriate risk-management techniques.

Indeed, with the purchase of options, while your profit potential is virtually unlimited, your risk is strictly limited to the small amounts you invest.

The third kind of leverage we use is not really leverage at all — even though it does offer the potential to go for astronomical gains quickly: Small-cap mining shares.

You simply buy their stock, no different than buying a share of Facebook or Google. But these companies’ values are tied at the hip to the price of the metal they produce.

In fact, during the last major gold rally, mining shares in this category rose to $68 for every $1 move in bullion!

And if, as we ex pect, the convergence of cycles send the value of industrial, energy and precious metals through the roof, small companies that mine them will likely do exponentially better.

Chapter 6

A Speculator’s Dream

We believe the next five years are going to be a speculator’s dream — not just for veteran speculators but for nearly ANY investor with the knowledge.

And as fear money rushes to the United States, it will likely turbocharge megatrends that are already beginning to take the world by storm. Here are just a few on Sean’s radar screen:

Massive defense spending: Unless peace breaks out suddenly (very unlikely despite Joe Biden’s handshake with Vladimir Putin in Geneva), massive future spending on defense is virtually unavoidable ...

And the last time this happened not long ago, historical market data shows us that select leveraged investments in one of his favorite defense companies posted gains of 329% in 195 days … 463% in 200 days … and 670%, also in 200 days!

That’s enough to multiply your wealth more than seven times over.

The mass conversion to electric cars: With the right timing, select speculative investments in Tesla could have given investors gains of 388% in 91 days, 579% in six months and 881% in just seven months.

That’s enough to turn every $10,000 into almost $991,000!

But our research proves that it’s not just the car companies that could make you rich. It’s the companies that develop the materials that make these vehicles possible.

Not long ago, leveraged investments on LIT, the lithium ETF, could have made you 231% in 91 days or a whopping 4,100% in just 5 months!

That’s enough to turn a $5,000 grubstake into a $205,000 fortune!

Shift to U.S. energy. In tandem with the shift of capital to the United States, we’ve seen a massive shift from Middle Eastern crude oil to U.S.-produced oil and natural gas.

By simply buying ordinary common stock in select companies like Marathon Oil, you could have seen gains of 45% in just 40 days.

But with judicious use of leverage, you could have seen gains of …

- 425% in 40 days …

- 1,422% in 42 days, and …

- 2,150% in 40 days — enough to turn a $10,000 investment into $225,000 in just over one month!

And here’s the BEST news:

All of our cycles research indicates that these megatrends are just beginning. The biggest profits will come during Phases Two, Three and Four of this crisis!

And because the timing of these megatrends is tied to predictable cycles, we have the confidence to use judicious leverage and go for the biggest reasonable gains possible.

All of these investments are perfect for Phase One of this crisis (now) and Phase Two. But when this great crisis strikes Washington D.C., we will make a major change of strategy …

You see, until that time, America will still be considered the safest safe haven in the world. So massive amounts of fear money will flow to our shores.

But after that time, investors everywhere will awaken to the fact that America is also feeling the sting of the crisis — that it is no longer a safe haven …

That it is, in fact, among the victims of the debt crisis.

At that point, it would be time to close out your positions on most U.S. investments and use inverse ETFs as well as put options to go for a third and final fortune in this crisis.

These would include funds like the ProShares UltraShort S&P 500 ETF … ProShares UltraShort QQQ ETF … ProShares Short Dow 30 ETF … and the ProShares UltraShort Russell 2000 ETF.

And you can also use options on these ETFs to go for gains of 400% … 500% and more.

When my father, Irving Weiss, saw a major depression on the way in the early 1930s, he borrowed $500 from his mother to follow a similar strategy. By the time the market hit rock bottom, he had transformed that small grubstake into $100,000, which is equivalent of $2 million in today’s dollars.

Two of his contemporaries, Jesse Livermore and Bernard Baruch, invested far larger sums and made the equivalent of billions of dollars.

In Phase Three of this crisis, thanks to our ability to time the markets with our cycle research, you should be able to follow a similar path — all with limited risk and by investing just a small portion of your money.

14 Supercycle Investment Opportunities

That Could Multiply Your Money in 2021—2026.

If everything plays out like our cycles are telling us …

In the next two phases of this crisis, we’re going for windfall profits of 500% or more as …

- Debt and war crisis drives trillions of dollars in flight capital into America’s most prosperous blue-chip companies.

- The crisis drives more money into companies that are leaders of sweeping megatrends — defense, electric cars and the U.S. energy boom.

- The Japanese yen and the euro resume their crash …

- And as Japanese and European stocks collapse.

In Phase Three, we aim to grow even richer as …

- The U.S. dollar crashes …

- Many U.S. stocks collapse …

- And as U.S. government bonds implode.

And throughout this crisis, we will go for still greater profits as this massive wave of flight capital drives precious metals and commodity prices through the roof in …

- Gold

- Silver

- Platinum

- Palladium

- Energy

- Food

- Industrial materials

And more!

Now, to help you survive and profit, we want to empower you to go to the next level.

Chapter 7

Immediate Access to Our “Buy”

and “Sell” Signals EVERY DAY

Throughout This Crisis!

This report may be enough to help you get through this. But we’re also giving you access to our “buy” and “sell” signals — if you’d like the timing information our cycles research produces:

Not just WHAT we’re recommending you buy or sell … but the precise moments WHEN you should act on each investment.

So, if you want to protect yourself and go for substantial profits with a minimum amount of work and no worry …

We have a solution I think you’ll like.

It’s Supercycle Investor — the service Sean Brodrick and I created to show you how to maximize your safety and profits as this great crisis strikes.

We built Supercycle Investor to help you

accomplish two very important objectives:

Objective #1: To protect every dollar you have saved and invested right now, so you can get through this with your wealth and financial security intact, and …

Objective #2: To help you harness the awesome power of this great crisis to grow even richer by going for windfall profits in each phase.

For starters — as soon as you join — you get …

- The Supercycle Investor Quick-Start Guide with everything you need to get the most out of your new membership — and to begin seizing supercycle profit opportunities right away.

- Unrestricted 24/7 access to the Supercycle Investor website where you can review all our issues, all our recommendations and view all our online video briefings any time you like.

- The Supercycle Email Hotline for quick answers to any questions you have about your membership or any recommendation we give you.

And you get so much more …

- You get Urgent Trading Alerts INSTANTLY whenever it’s time for you to make a move.

Once you decide that the trade is right for you. You will have all the information you need on what to buy, why to buy it, when to buy it, how much to pay and how much money we think you stand to make on the trade.

And whether it’s an individual stock, a garden-variety ETF, an inverse ETF, a leveraged ETF or an option on an ETF, Sean gives you everything you need in plain English.

You’ll get step-by-step instructions on how to make the trade online or on the phone with your broker. If you want, you could simply call your broker and read the Trading Alert aloud on the phone.

Ditto for when it’s time to sell. We’ll make sure you have everything you need to make the trade quickly, easily and with confidence.

THE BOTTOM LINE: We will never leave you hanging. You will never be left wondering what you should do. If you can read an alert and dial the phone (or make trades online), all the profits this opportunity offers you are within your grasp!

- You get regular updates in weekly issues of Supercycle Investor.

Each issue of this weekly letter will keep you up to date on every investment we own as well as the global developments that are impacting them.

Plus, we’ll also use this forum to answer the questions we’re getting most often by our members.

- You’ll meet with us for LIVE online strategy sessions every quarter.

At these hour-long meetings, we’ll show you what we’re seeing in the charts, and you’ll see how actual events on the ground are bearing out our cyclical forecasts.

And since these events will be LIVE, you can ask us anything you like about the investments or strategy we recommend as well as our views on breaking events ...

Also, we’ll meet for live online emergency summits when warranted.

I am so confident in our forecasts …

So concerned that you protect yourself …

And so eager to help you go for your share of the windfall opportunities that will be available as this supercycle courses through the global economy …

I will gladly pay most of your

membership fee for you.

Normally, Supercycle Investor retails for $3,000 per year.

But here’s the thing: The cycles driving this crisis say it’s going to be with us for five years — until 2022. And five years times $3000 per year would be $15,000.

That’s more than fair if you think about it. After all, your first winning trades alone could deliver a lot more than $15,000.

But frankly, a $15,000 price tag for a five-year membership could deprive good people of the recommendations they need to protect themselves and profit.So, after much soul-searching and pencil-sharpening, here’s what I’ve decided to do:

If you click here and join us for just two years now, I will pay

for the remaining four years of your 5-year membership.

YOU SAVE A

|

|

| 2-year membership: | $6,000 |

| Your bottom-line cost: | $2,945 |

| Immediate savings: | $3,055 |

| 3 MORE years FREE: | $9,000 |

| Your total savings: | $12,055 |

CLICK HERE or (Phone orders: 8:30-5:30 EST) |

|

I sharpened my pencil and — for this Introductory offer only — slashed the annual rate so you can get two years for just $3,945.

Plus, since you are already a Weiss subscriber, you are entitled to an ADDITIONAL discount of a full $1,000! Your bottom-line cost is only $2,945!

And that’s just the beginning of the savings you reap because …

We will pay for you to receive three MORE years — a $9,000 value — FREE.

Add it all up and it means you save a total of $12,055 in breaks just for joining now!

You get FIVE full years of Supercycle Investor — all the time you need to protect and grow your money through the end of this five-year Supercycle.

So, your Supercycle Investor is a mere $1.61 per day — half the price of one gallon of gasoline — and you get news, analysis and “Buy” and “Sell” signals designed to multiply your wealth many times over.

With these deep discounts, your very first profitable trade could easily pay for your entire membership many times over!

Plus, there’s more:

You must be thrilled with the money you make,

or you can get a refund for any reason,

anytime in the next year.

You don’t even have to make your final decision now. You can wait until then to do that.

Click here to join us and I’ll pay for THREE years of your five-year membership. Then, just follow our recommendations for the next few weeks, the next few months, or even for a full year.

In the unlikely event that you decide Supercycle Investor isn’t right for you, just let us know any time within your first year, and I’ll promptly give you a refund on the balance of your subscription.

That way, I take virtually all the risk out of your membership. Either our forecasts prove accurate now and you make a lot of money … or you can cancel and get a refund.

This is THE watershed moment

of your financial life.

Your entire life as an investor — and as a student of the economy and the investment markets — has led you to this moment.

You’ve always known that the obscene debts our leaders were amassing were unsustainable.

You always knew that sooner or later, the end of this great debt cycle would come to an end one day — and that there would be hell to pay.

Now, the same cycles that accurately predicted the roaring 1920s, the Great Depression — and every major economic or investment event since — are converging to form a powerful new supercycle …

A supercycle that marks the end of the era in which our leaders could amass mountains of debt with impunity …

And the beginning of a dangerous new era in which we all pay the price for that debt.

As we’ve seen, the facts on the ground are in synch with this forecast. They confirm and validate every warning our cycles research is giving us.

The die is cast. The handwriting is on the wall.

These facts leave us with two choices — and ONLY two:

We can do nothing while knowing full well that these events could destroy nearly everything we have worked for.

Or, we can do what is necessary to protect our wealth — and better yet, harness the awesome power of these events — to go for windfall profits with stocks, ETFs, leveraged ETFs and even some options.

Please remember what’s at stake: Well before the worst of this crisis began — many of these investments could have posted actual, real-world profits of …

719%, 1,076% and 1,214% (industrial metals) …

1,260%, 1,275% and 1,536% (metals used for energy), plus …

1,422%, 2,150% and 4,100% (electric vehicles).

But starting now, the convergence of cycles will threaten to wipe out millions of investors who fail to prepare … and send the investments we’ve named in this report into high gear, with the potential to make you several fortunes.

I’ve made my choice. I’m doing what’s necessary to protect my family’s wealth.

I urge you to do the same.

In my view, you have nothing to lose and everything to gain:

Go here to subscribe now.

Or call us toll-free at 855-278-9191 (8:30 to 5:30 EST).

Remember: I am so confident in this forecast … so concerned that you protect yourself … and so eager to help you go for your share of the windfall profit opportunities that this supercycle is making available to you … I will gladly pay for four-fifths of your five-year membership fee.

Plus, with my refund guarantee, I take virtually all the risk on the cost of your subscription.

That should tell you something about how committed I am to making this work for you.

Please let me hear from you right away: These unusual Introductory Member savings EXPIRE very soon.

Sean and I look forward to welcoming you aboard.

Good luck and God bless!

Martin D. Weiss, PhD

Founder, Weiss Ratings

with

Sean Brodrick

Senior Analyst and

Economic Cycles Specialist