We’re just beginning to unwind one of the biggest, broadest financial bubbles in the history of the world.

The system was already so pumped up by debt-fueled speculation and easy money, it was just waiting for a pin. And along came a Tomahawk cruise missile!

In the more than three decades since I began my journey as a stock market analyst, I’ve seen my share of panics.

Folks ask me if the 2008 crisis was as grim as the disaster we face today.

No.

There were only a few dozen financially diseased large companies around the world, and the governments of the richest countries were ultimately able to bail them out.

This time, virtually every business and every bank in every country is getting sucked into the vortex. We can’t predict the future, but it will be very difficult for governments to rescue them all.

Others wonder if the Crash of 1929 and the Great Depression that followed were worse.

Not likely.

During the Great Depression, the U.S. unemployment rate never exceeded 25%, and it took many months to reach its peak.

St. Louis Federal Reserve President James Bullard predicts the unemployment rate may soon hit 30% … and 30 million American workers have already filed for unemployment insurance amid shutdowns to combat the coronavirus.

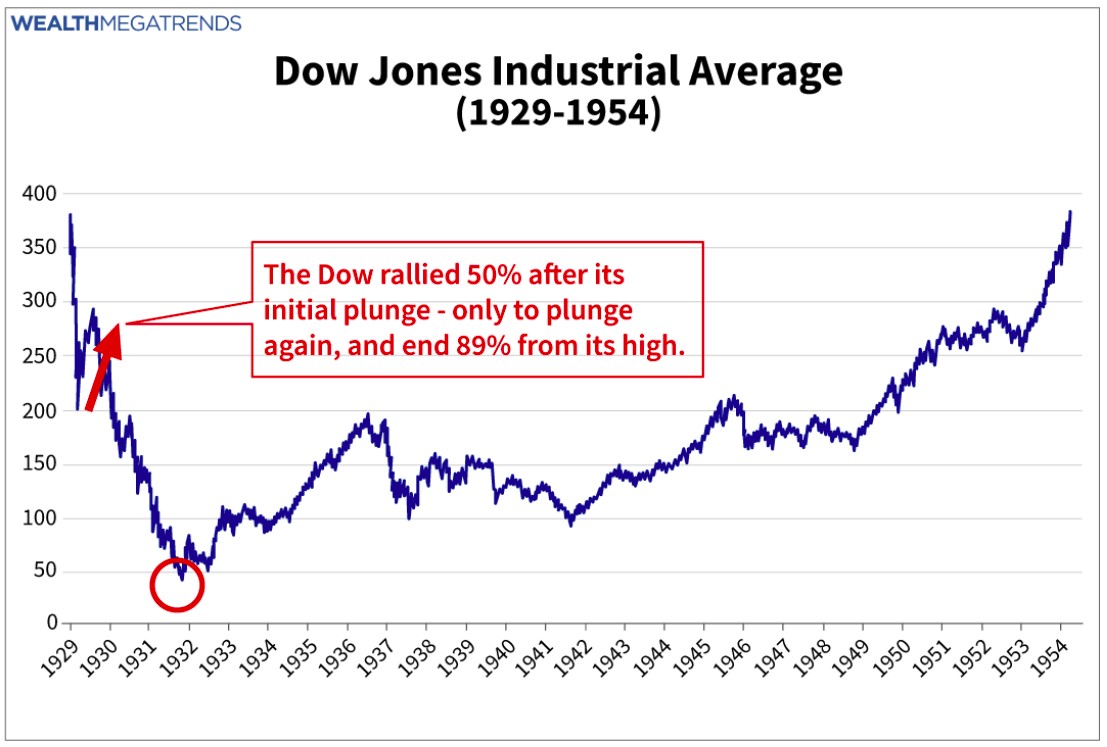

For what we can expect in the weeks ahead, look at this chart of the Dow Jones Industrial Average during the Great Depression …

In the fall of 1929, the market fell nearly 50%. Then, starting in late 1929 it rallied through April of 1930.

In fact, it rallied 50%, to a level only 20% below its high.

But it crashed again. Worse than the first time.

Eventually, the bear market hit rock bottom with a devastating decline of 89%. The market did not recoup to its old high again for another quarter of a century.

Now take a deep breath. Panic never helped anyone. But neither does complacency.

Here’s a story that might give you some hope …

In April of 1930, as the Dow’s post-crash rally was peaking, our founder’s father, J. Irving Weiss, found a way to PROFIT from the bear market. He borrowed $500 from his mother … shorted stocks he felt were the most vulnerable … and by 1932 had over $100,000 (about $2 million in today’s dollars).

But he also took extreme and unlimited risks.

Nowadays, there are easier and less risky ways to “short” the market.

“Inverse ETFs” that RISE in value when an index FALLS.

These types of ETFs can rise 1% for every 1% decline. Or they can be leveraged — rising 2% or even 3% for every 1% fall in the index.

Some liquid inverse stock ETFs include …

ProShares Short S&P 500 (NYSE: SH). This fund tracks the inverse of the daily performance of the S&P 500. It has an expense ratio of 0.89%

ProShares Short Dow30 (NYSE: DOG). This fund tracks the inverse of the daily performance of the Dow Jones Industrial Average. It has an expense ratio of 0.95%.

Some inverse Bond ETFs include …

ProShares Short 20+ Year Treasury (TBF). This inverse ETF is designed to move inversely to the Barclays U.S. 20+ Year U.S. Treasury Bond Index. If the deficit blows out, government bond issuance soars and investors panic over Uncle Sam’s balance sheet … this ETF will protect you. That’s because bond prices will plunge as interest rates soar.

ProShares Short High Yield (SJB). This inverse ETF doesn’t target Treasury prices. It’s designed to move inversely to the Markit iBoxx $ Liquid High Yield Index … a benchmark index for JUNK bonds.

SJB is probably your best bet for the foreseeable future …

Given the enormity of the corporate credit bubble, junk and corporate bonds are likely to sell off first … plowing their money into treasuries as a “Safe Haven” … driving their prices UP.

Inverse ETFs are more appropriate for shorter-term trades. Days to weeks for leveraged ones. A few months at most for unleveraged versions.

And only buy the most liquid inverse ETFs: You want to be able to get in and out without getting hosed.

Since February, my subscribers have seen gains of 2.39% in four days … 10% in 11 days … even 46% in 13 days.

Not all trades were gains, but the average trade was up 13.7% in well under a month!

And have you noticed the Dow has retraced over 50% of March’s drop? And that it’s (again) about 20% off its high? Is it 1929 all over again?

Only time will tell. But I think playing it safe with an inverse ETF is a solid plan.

All the best,

Sean